- English

- عربي

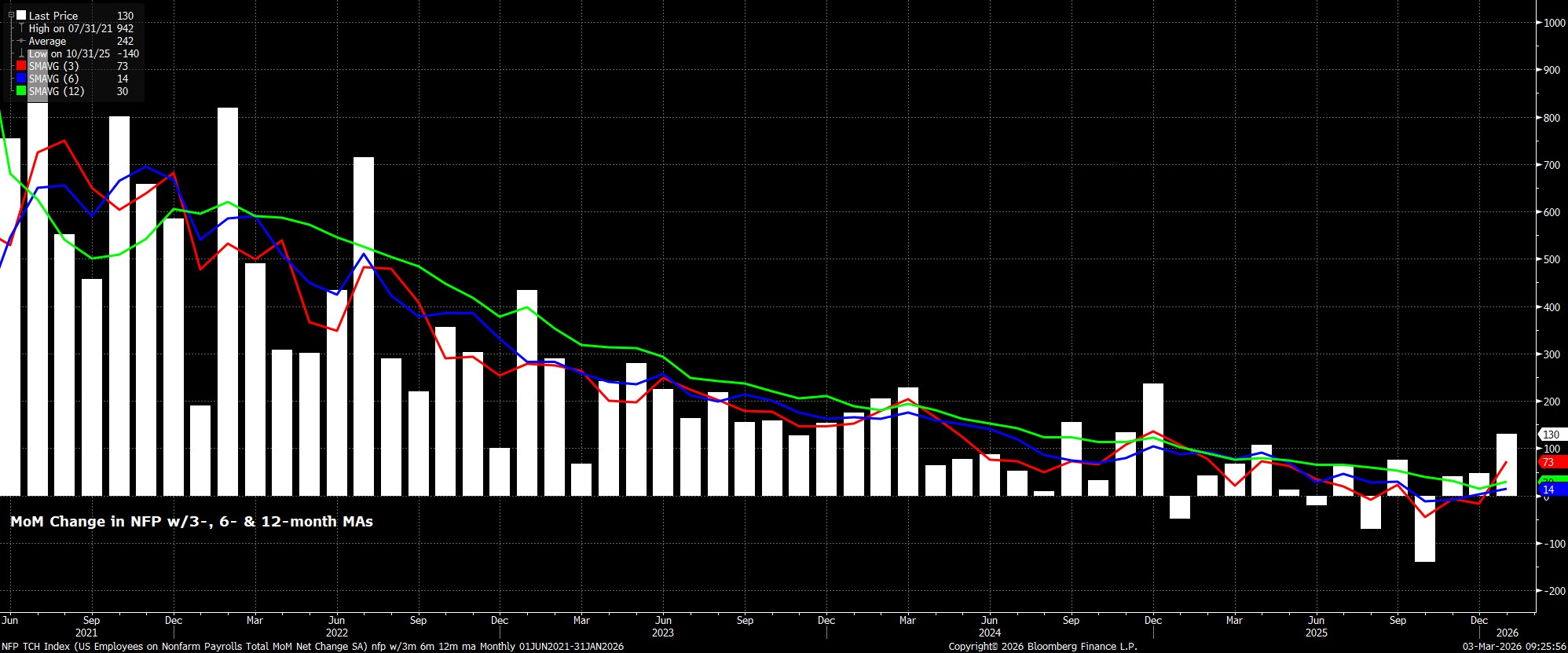

Payrolls Growth Set To Moderate

Headline nonfarm payrolls are set to have risen by +60k last month, a sharp moderation from the above-consensus +130k increase seen in January, albeit a rate that would be broadly in line with the breakeven pace of job creation.

That said, not only is the range of estimates for the payrolls print as wide as usual, from -10k to +115k, one must also recall that data quality issues continue to impact the print, potentially leading to job creation being overstated by as much as 60k, per Chair Powell. Hence, participants and policymakers alike are set to mentally revise down the headline figure by that magnitude, in order to gain a truer read on the labour backdrop.

Downside Risks To Consensus

Furthermore, on balance, risks to the aforementioned headline print appear to tilt to the downside, with the January payrolls print also at risk of being revised lower, as has tended to be the case in recent years.

As for the February figure, weather is the chief concern in terms of downside skew, considering the brutal cold snap that the US endured in late-January and early-February. While the bulk of that inclement weather had cleared by the time of the survey week, there is nonetheless still likely to be some impact felt on weather-sensitive sectors, with construction being the most notable area to watch on this front.

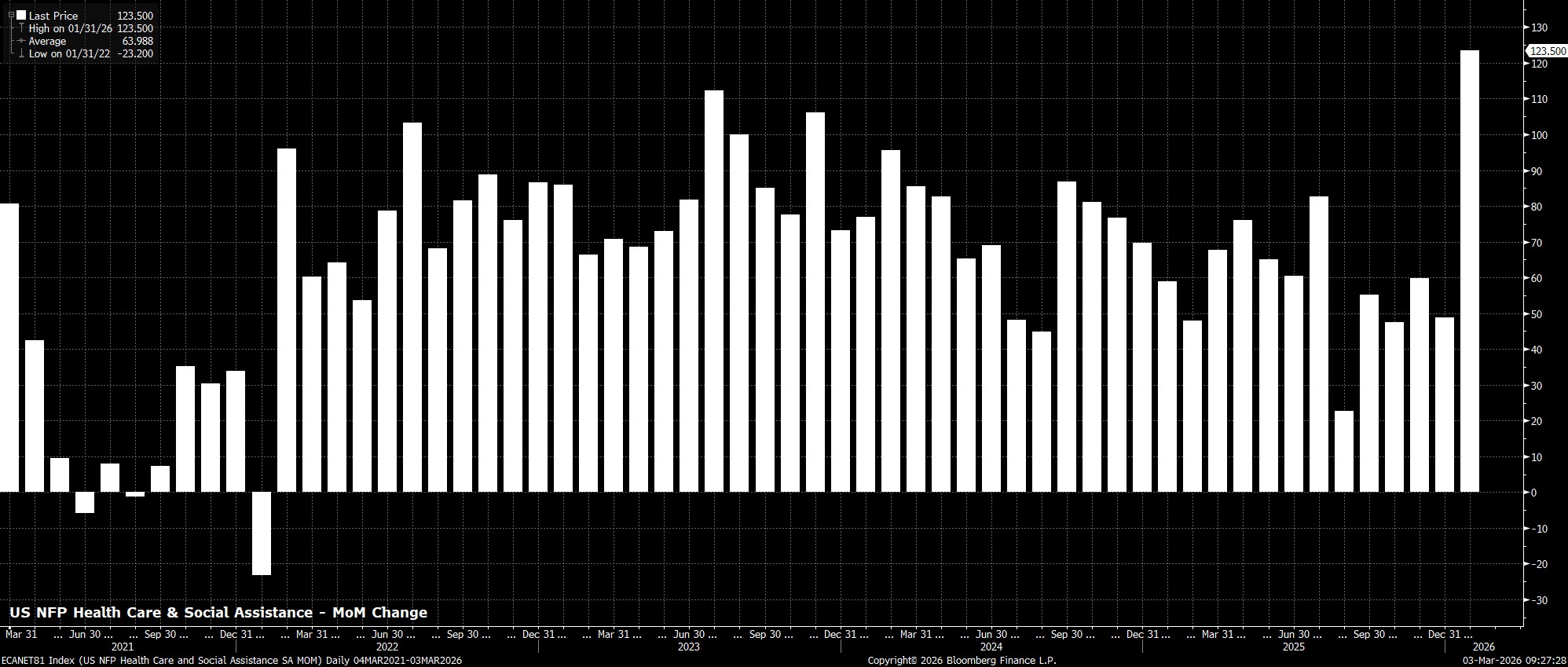

Meanwhile, healthcare employment rose by +124k in January, not only double the pace seen on average over the preceding twelve months, but also the largest MoM gain in employment in the sector seen in at least five years. It seems implausible to expect that demand for healthcare workers has increased by such a huge margin, in such a short space of time, likely leading to a degree of mean reversion in the February report.

As for government employment, the impact of last year’s deferred resignation programme has probably now entirely made its way through the payrolls data, while the mid-February DHS shutdown came after the end of the reference week. Still, an ongoing federal hiring freeze should continue to act as a drag here.

Leading Indicators Lean The Other Way

While those factors point to downside risks, leading indicators for the headline payrolls print tell a different story.

Initial jobless claims were essentially unchanged between the January and February survey weeks, while continuing claims rose a modest +14k over the same period. Elsewhere, the NFIB survey pointed to a pick-up in hiring intentions, and the weekly ADP metric, albeit for the week prior to the reference week, signals a jobs gain of +51k, having continued to accelerate in recent weeks. PMIs are also painting a somewhat rosier picture, with the ISM manufacturing survey’s employment sub-index rising to its highest levels in over a year at 48.8 last month, though the equivalent services metric has yet to be released at the time of writing.

Earnings Pressures To Stay Contained

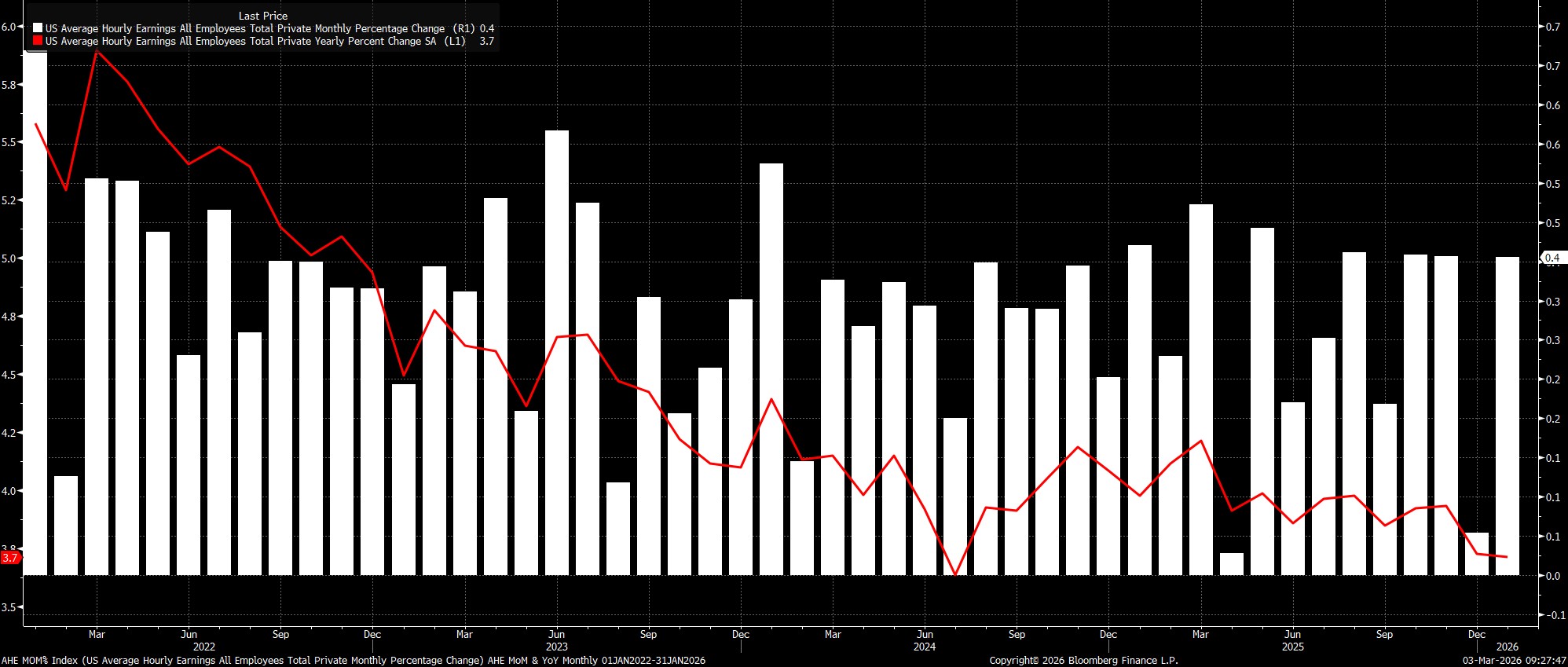

Staying with the establishment survey, the jobs report is set to show wage pressures remaining contained, with average hourly earnings set to have dipped 0.1pp to 0.3% MoM in February, seeing the annual rate remain unchanged at 3.7% YoY. The workweek is also set to remain unchanged, at 34.3 hours.

Data of this ilk, clearly, is likely to be of little concern to the FOMC, with pay pressures not threatening the sustainable achievement of the 2% inflation aim over the medium-term at the present time.

Household Survey Of Greater Importance

Turning to the household survey, data here remains of considerably more importance in terms of the Fed policy outlook, not only given Chair Powell’s aforementioned comments regarding the accuracy of the headline payrolls figure, but also as policymakers attempt to gauge the degree of slack present within the labour market.

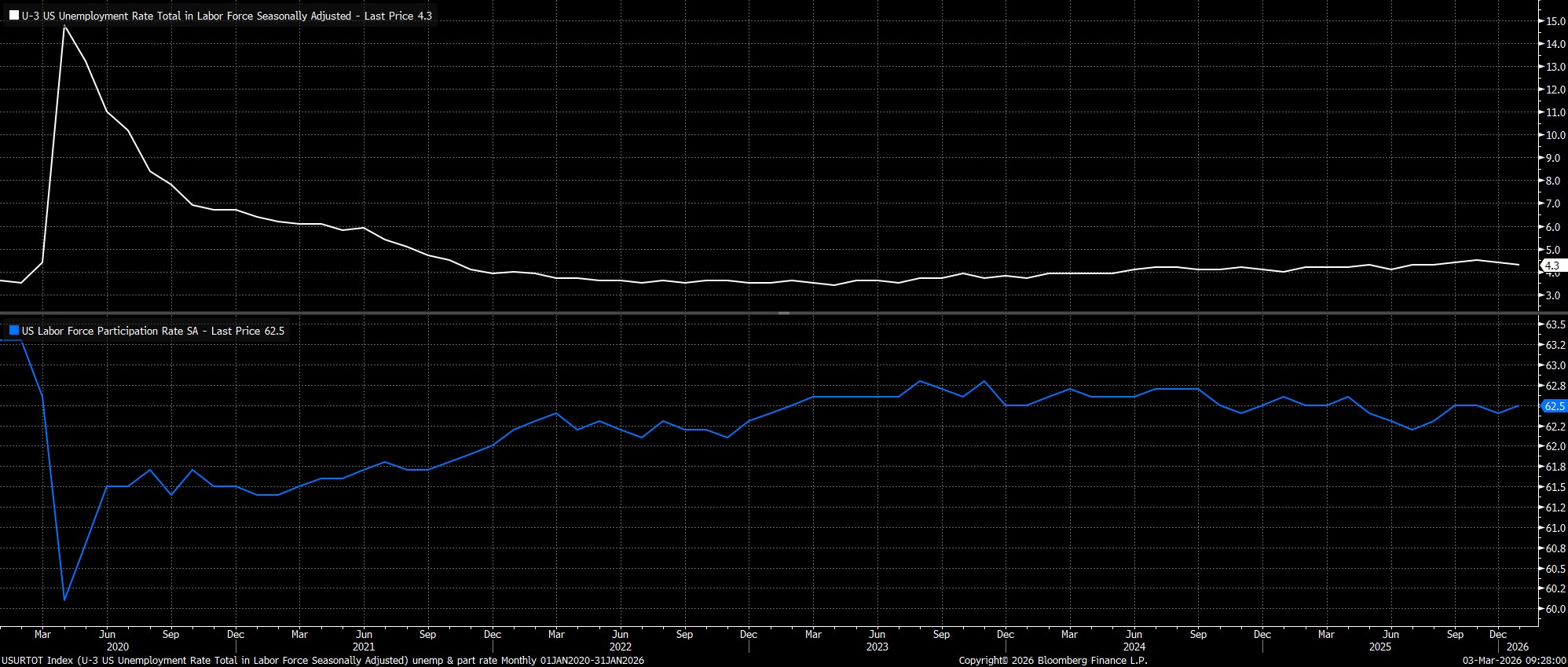

Headline unemployment is set to have held steady at 4.3% in February, remaining 0.2pp off the cycle highs seen last November. In fact, with January’s unrounded U-3 rate having been 4.2832%, there is a relatively high bar for unemployment to tick higher on a rounded basis this time out.

Labour force participation, meanwhile, is set to have held steady at 62.5%, though this remains some 0.3pp off the 62.8% cycle high seen during summer 2023.

Limited Policy Implications

Taking a step back, the February jobs report seems unlikely to materially ‘move the needle’ in terms of the near-term FOMC policy outlook.

The Committee adopted a ‘wait and see’ stance at the January confab signalling a belief that an ample amount of ‘insurance’ has been taken out against downside labour risks, courtesy of the 175bp of cuts delivered since the easing cycle begun in September 2024. In fact, even Governor Waller, who dissented for a 25bp cut in January, recently signalled that he would be prepared to vote for rates to remain unchanged if the February jobs report is as robust as the prior one.

Waller, and uber-dovish Governor Miran, aside, the remainder of the FOMC appear happy to stand pat for the foreseeable regardless, with the base case now being that no further cuts are delivered with Chair Powell at the helm, barring a material downside surprise to the outlook. Such a base case is reinforced by recent geopolitical tensions in the Middle East, with policymakers set to closely monitor the potential inflationary impact of any energy price shocks.

That said, further rate reductions remain on the cards later in the year, with the disinflationary process likely to continue, and in any case policymakers tending to ‘look-through’ the impact of short-term commodity price swings, retaining a focus on the underlying inflation backdrop. Chair designate Warsh, though, barring a significant deterioration in labour conditions, or a return to the 2% inflation target, could well have some difficulty in convincing his new colleagues on the FOMC to adopt as dovish an approach as we’ve been led to believe that he is likely to seek.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.