- English

- 中文版

A Virtuous Cycle For Equities May Be A Vicious One For Labour

The Stock Market Is Not The Economy

It’s a well-worn adage that ‘the stock market is not the economy’.

Over time, that adage has tended to ring true more often than not. Equities operate as a forward-looking discounting mechanism, pricing expectations of future corporate earnings, as opposed to whatever the economic reality ‘on the ground’ may be in the here and now.

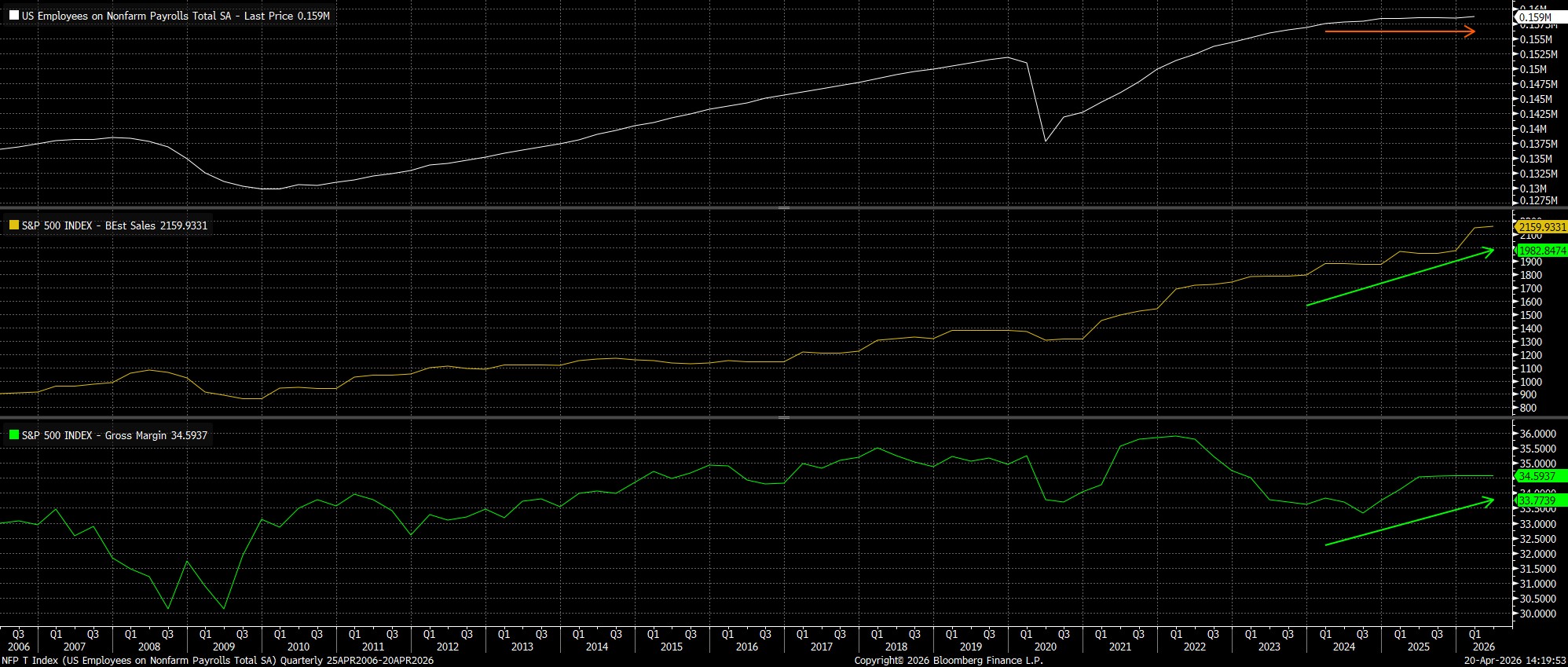

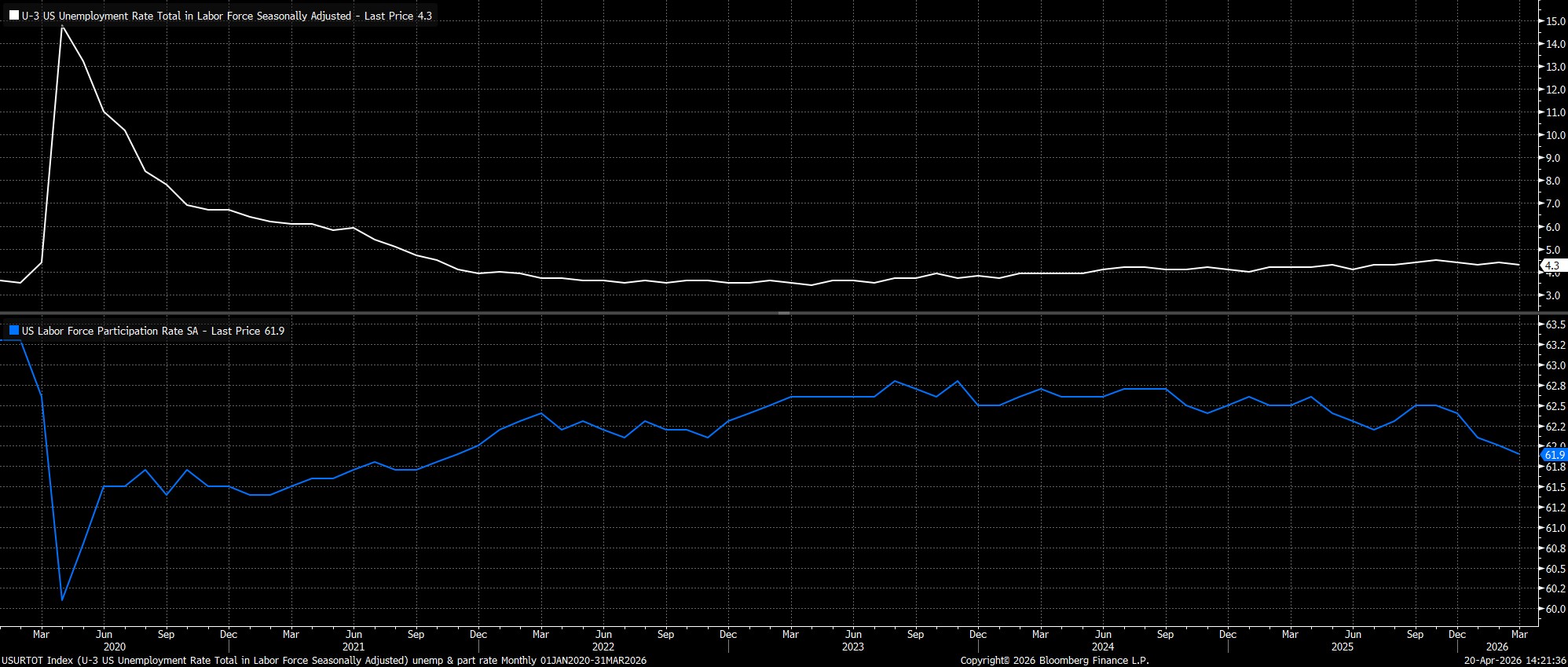

There have, perhaps, seldom been many times where that divergence has been as stark as it is now. Not only from a geopolitical perspective, where major Wall St benchmarks trade at all-time highs, despite conflict continuing to rage, but from an economic one too, with stocks at record highs, while consumer sentiment plumbs record lows, and the labour market remains mired in a ‘no hire, no fire’ dynamic.

So, what’s driving the equity market higher?

Put simply, there seems to be something of a virtuous cycle going on here. Increasingly, it is the case that corporates are able to grow revenues, substantially in some cases, while keeping labour costs largely unchanged, or even reducing them via layoffs, in turn resulting in a lower cost of goods sold, and a higher gross margin. Arguably the only factor that can explain this dynamic is higher productivity, whereby either fewer workers are producing the same level of output, or the same number of workers are producing more output.

Importantly, this apparent higher productivity is coming, by and large, before the impacts of increased automation, and increased AI adoption, make themselves known.

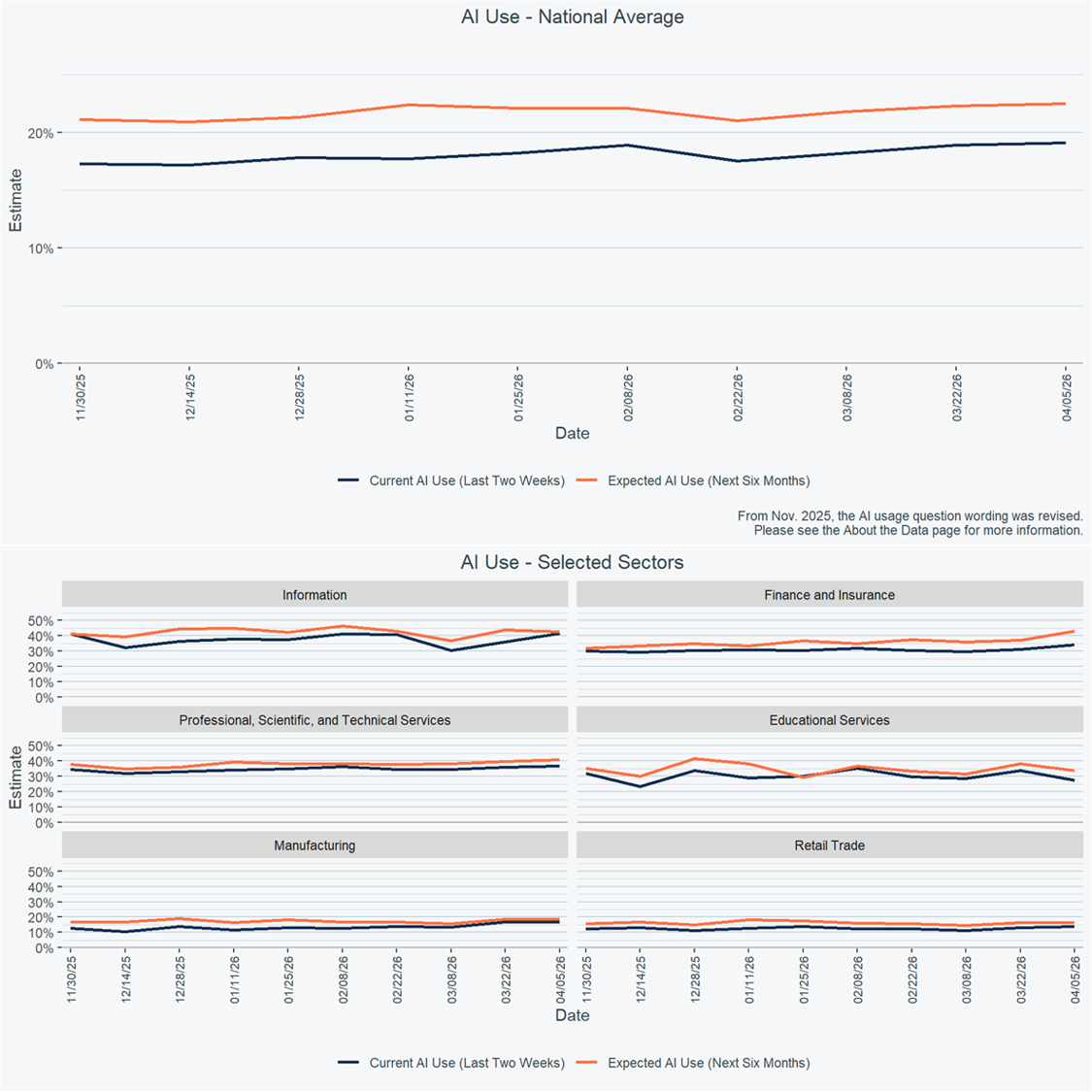

According to the most recent ‘Business Trends and Outlook Survey’, from the US Census Bureau, only around 20% of respondents noted that their business had used AI in any function over the last two weeks, while around 23% noted that the planned to do so in the next six months. While AI adoption varies considerably across sectors, with almost half of Finance and Insurance businesses surveyed having adopted AI already, compared to around 10% of Retail firms, the overall picture being painted here is one where AI adoption has significantly more room to run, in turn allowing the aforementioned virtuous cycle that is currently driving the market, to continue doing so.

Buybacks Play A Role Too

Concurrently, there is increasingly a shortage of stock that is actually available for investors to buy.

Across the board, corporates have ramped-up buybacks in recent years and, while I view this as one of the most inefficient conceivable uses of capital, the amount of stock being bought back shows no sign of slowing. The total S&P 500 buyback topped $1tln in 2025, with this year likely to see a similarly strong pace of corporate repurchases. Going back to our ‘Economics 101’ textbooks, we know that, all else equal, if the supply of a good (in this case a stock) were to decline, and demand to remain unchanged, or even increase, a higher price of the good, or stock, in question is the ultimate result. Again, as the pace of buybacks continues, so does the equity market’s virtuous cycle.

_SPX_Bu_2026-04-20_14-21-19.jpg)

A Net Negative For Employment

While all this marks a ‘virtuous cycle’ for equities, which looks set to continue for some time, one could argue that it marks something of a ‘vicious cycle’ for employees.

This isn’t a particularly groundbreaking take, but as productivity increases, either as a result of AI, or some other factor, corporates are likely to operate somewhat leaner business models, with lower headcount. Already, the labour market backdrop is a relatively fragile one, with a broader shift to such a model likely to further embed the already-lacklustre nature of labour demand.

Perpetuating The 'K-Shaped' Economy

Taking this a step further, it seems plausible that, together, these two factors – a virtuous cycle for stocks, and a vicious one for employment – will further perpetuate the idea of a ‘K-shaped’ US economy.

To recap, this is one where those who own assets, either property or stocks, sit in the top part of the ‘K’, benefitting from a positive wealth effect, and in turn largely propping up overall personal consumption. Simultaneously, those in the lower part of the ‘K’, who tend not to be asset owners, experience a very different economy, whereby the weak employment backdrop has a much more detrimental impact on consumption. Of course, ballooning government deficits, and a monetary policy framework which has implicitly accepted 2% inflation as a floor not a ceiling, don’t help matters much on this front.

Summing up, it’s clear that the stock market is not the economy; in many ways, for the sake of equity bulls, it’s just as well that that is the case.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.