Share

八月末将至,夏季也即将结束,尽管今年市场并没有出现典型的夏季低迷,资产类别间的拥挤交易却异常波动。然而,随着一些宁静的降临,现在正是展望年底可能带来的交易机会,以及在外汇领域可能出现的关键交易机会的时候。

2024年的大部分时间,G10外汇市场相对平静,交易区间狭窄,隐含波动率和实现波动率均处于极低水平,但在夏季市场活跃起来。首先,参与者不得不消化日本央行比预期更加鹰派的决定,这激发了广泛的套利交易解除。随后,七月份美国就业报告疲软,加上美联储主席鲍威尔在杰克逊霍尔意外的鸽派讲话,几乎确认了9月份的降息,导致美元跌至年内最低水平。

这为市场在夏季结束时回归更正常活动水平铺平了道路。

从现在到年底,两个关键因素似乎可能影响外汇市场。一是货币政策的发展,随着大部分G10国家继续正常化,以及日本央行进一步加息的可能性;二是即将到来的美国总统大选,随着白宫竞选热度升温,尽管下议院选举也将受到关注。

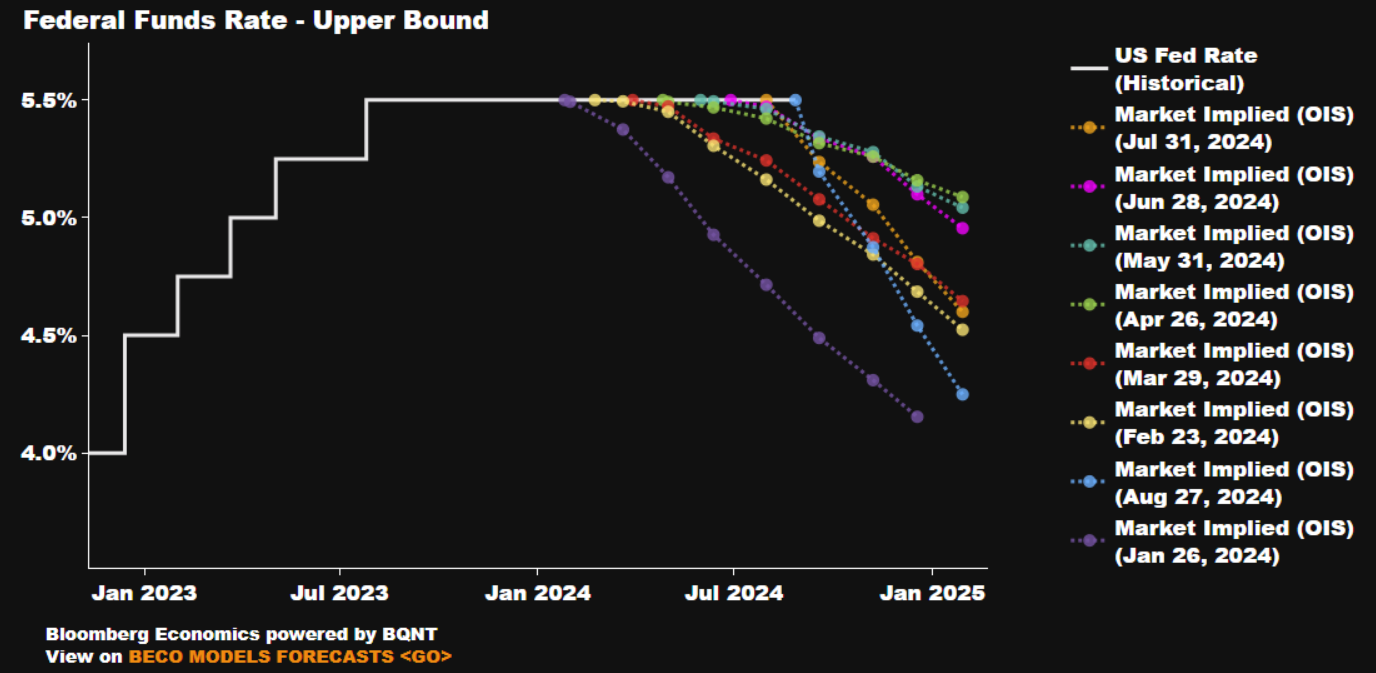

货币政策动态可能以几种方式影响市场。首先,市场对降息的定价是谁会达到,谁不会达到。例如,美联储已经设定了一个非常高的门槛,以满足市场对年底前约100个基点宽松的预期,除非有重大外部冲击,否则这似乎是不切实际的。因此,美元存在上涨风险。尽管整体上各国的利率定价都很雄心勃勃,但英镑(年底前降息40个基点)、瑞典克朗(年底前降息75个基点)和瑞士法郎(年底前降息49个基点)似乎更为合理定价,因此可能处于脆弱地位。

这为市场在夏季结束时回归更正常活动水平铺平了道路。

从现在到年底,两个关键因素似乎可能影响外汇市场。一是货币政策的发展,随着大部分G10国家继续正常化,以及日本央行进一步加息的可能性;二是即将到来的美国总统大选,随着白宫竞选热度升温,尽管下议院选举也将受到关注。

货币政策动态可能以几种方式影响市场。首先,市场对降息的定价是谁会达到,谁不会达到。例如,美联储已经设定了一个非常高的门槛,以满足市场对年底前约100个基点宽松的预期,除非有重大外部冲击,否则这似乎是不切实际的。因此,美元存在上涨风险。尽管整体上各国的利率定价都很雄心勃勃,但英镑(年底前降息40个基点)、瑞典克朗(年底前降息75个基点)和瑞士法郎(年底前降息49个基点)似乎更为合理定价,因此可能处于脆弱地位。

Preview

其次,还有一个问题,即尚未降息的那些中央银行 - 即澳洲联储和挪威中央银行 - 将维持这些“更高更久”立场多久。以最近的言论为准,目前看来,2024年澳洲联储和挪威中央银行的降息似乎遥不可及,尽管在鲍威尔等人开始降低联邦基金利率之后,这种立场能否持续尚存疑问。如果是这样,那么澳元和挪威克朗将成为G10外汇市场中明显的多头,可能会在风险情绪继续保持的情况下对低收益货币获得最显著的益处

最后,有一个不确定因素,那就是日本央行。在7月传递出比预期更加鹰派的信息后,宣布上调15个基点并计划削减日本国债购买的上田行长留下了进一步紧缩的可能性,同时指出0.5%并非利率的“上限”。日元OIS曲线价格显示,到年底只有11个基点的进一步收紧,这似乎有些不足,为日元升值留下了空间,因为日本与其他地区的利率差继续收窄,即使套利解除似乎在目前阶段基本完成

除了政策,市场还需要应对美国大选的问题。在对金融市场重要的政策领域 - 例如财政政策 - 特朗普和哈里斯展示出了惊人的相似之处; 主要是,二者都不太关心更高的政府支出、不断上升的赤字或激增的政府借款。最重要的政策差异出现在监管领域 - 特朗普支持放松监管,哈里斯基本支持对美国企业实行更严格的规定 - 尽管这些差异的市场影响主要将在股票领域展现出来,而不是在外汇市场上

最后,有一个不确定因素,那就是日本央行。在7月传递出比预期更加鹰派的信息后,宣布上调15个基点并计划削减日本国债购买的上田行长留下了进一步紧缩的可能性,同时指出0.5%并非利率的“上限”。日元OIS曲线价格显示,到年底只有11个基点的进一步收紧,这似乎有些不足,为日元升值留下了空间,因为日本与其他地区的利率差继续收窄,即使套利解除似乎在目前阶段基本完成

除了政策,市场还需要应对美国大选的问题。在对金融市场重要的政策领域 - 例如财政政策 - 特朗普和哈里斯展示出了惊人的相似之处; 主要是,二者都不太关心更高的政府支出、不断上升的赤字或激增的政府借款。最重要的政策差异出现在监管领域 - 特朗普支持放松监管,哈里斯基本支持对美国企业实行更严格的规定 - 尽管这些差异的市场影响主要将在股票领域展现出来,而不是在外汇市场上

Preview

在外汇领域,人们预计特朗普的胜利对美元将是一个膝跳式的积极影响,即使只是机械性地由于墨西哥比索和人民币兑美元的显著贬值。然而,外汇市场通常更关心政治稳定,而不是政府的特定效忠,这意味着一个分裂的政府情景——即赢得白宫的党派并没有总体控制国会——可能是最重要的短期负面美元结果。总的来说,正如“自上帝还是个男孩以来”一直如此,市场在准确定价政治风险方面一直不佳。因此,预期波动率和实现波动率可能会在11月的投票日大幅上升,同时外汇需求也可能加速增长,因为交易员寻求对其他地方的政治敏感头寸进行对冲。

此处提供的材料并未按照旨在促进投资研究独立性的法律要求准备,因此被视为市场沟通之用途。虽然在传播投资研究之前不受任何禁止交易的限制,但我们不会在将其提供给我们的客户之前寻求利用任何优势。

Pepperstone 并不表示此处提供的材料是准确、最新或完整的,因此不应依赖于此。该信息,无论是否来自第三方,都不应被视为推荐;或买卖要约;或征求购买或出售任何证券、金融产品或工具的要约;或参与任何特定的交易策略。它没有考虑读者的财务状况或投资目标。我们建议此内容的任何读者寻求自己的建议。未经 Pepperstone 批准,不得复制或重新分发此信息。