差價合約(CFD)是複雜的工具,由於槓桿作用,存在快速虧損的高風險。81.1% 的散戶投資者在與該提供商進行差價合約交易時賬戶虧損。 您應該考慮自己是否了解差價合約的原理,以及是否有承受資金損失的高風險的能力。

- 繁体中文

- 简体中文

- English

- Español

- Tiếng Việt

- Português

- لغة عربية

- ไทย

- 繁体中文

- 简体中文

- English

- Español

- Tiếng Việt

- Português

- لغة عربية

- ไทย

Share

八月末將至,夏季也即將結束,盡管今年市場並沒有出現典型的夏季低迷,資產類別間的擁擠交易卻異常波動。然而,隨著一些寧靜的降臨,現在正是展望年底可能帶來的交易機會,以及在外匯領域可能出現的關鍵交易機會的時候。

2024年的大部分時間,G10外匯市場相對平靜,交易區間狹窄,隱含波動率和實現波動率均處於極低水平,但在夏季市場活躍起來。首先,參與者不得不消化日本央行比預期更加鷹派的決定,這激發了廣泛的套利交易解除。隨後,七月份美國就業報告疲軟,加上美聯儲主席鮑威爾在傑克遜霍爾意外的鴿派講話,幾乎確認了9月份的降息,導致美元跌至年內最低水平。

這為市場在夏季結束時回歸更正常活動水平鋪平了道路。

從現在到年底,兩個關鍵因素似乎可能影響外匯市場。一是貨幣政策的發展,隨著大部分G10國家繼續正常化,以及日本央行進一步加息的可能性;二是即將到來的美國總統大選,隨著白宮競選熱度升溫,儘管下議院選舉也將受到關注。

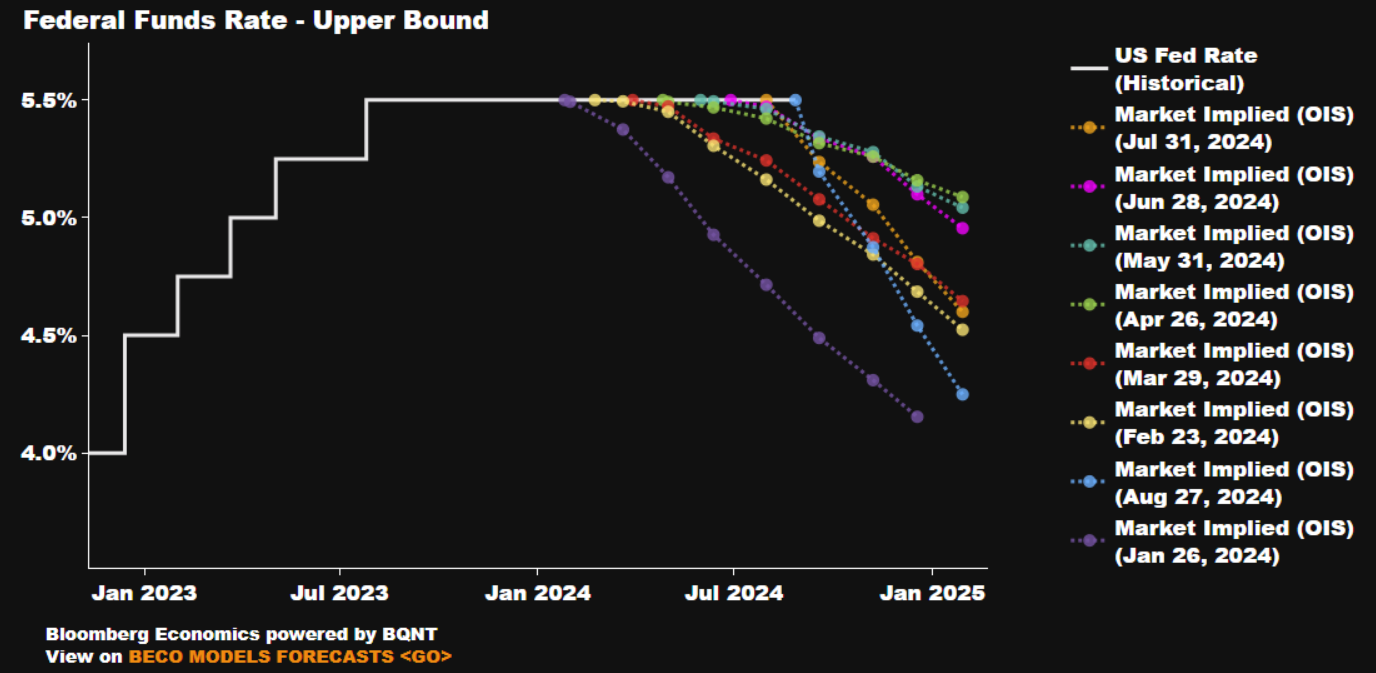

貨幣政策動態可能以幾種方式影響市場。首先,市場對降息的定價是誰會達到,誰不會達到。例如,美聯儲已經設定了一個非常高的門檻,以滿足市場對年底前約100個基點寬鬆的預期,除非有重大外部衝擊,否則這似乎是不切實際的。因此,美元存在上漲風險。儘管整體上各國的利率定價都很雄心勃勃,但英鎊(年底前降息40個基點)、瑞典克朗(年底前降息75個基點)和瑞士法郎(年底前降息49個基點)似乎更為合理定價,因此可能處於脆弱地位。

這為市場在夏季結束時回歸更正常活動水平鋪平了道路。

從現在到年底,兩個關鍵因素似乎可能影響外匯市場。一是貨幣政策的發展,隨著大部分G10國家繼續正常化,以及日本央行進一步加息的可能性;二是即將到來的美國總統大選,隨著白宮競選熱度升溫,儘管下議院選舉也將受到關注。

貨幣政策動態可能以幾種方式影響市場。首先,市場對降息的定價是誰會達到,誰不會達到。例如,美聯儲已經設定了一個非常高的門檻,以滿足市場對年底前約100個基點寬鬆的預期,除非有重大外部衝擊,否則這似乎是不切實際的。因此,美元存在上漲風險。儘管整體上各國的利率定價都很雄心勃勃,但英鎊(年底前降息40個基點)、瑞典克朗(年底前降息75個基點)和瑞士法郎(年底前降息49個基點)似乎更為合理定價,因此可能處於脆弱地位。

Preview

其次,還有一個問題,即尚未降息的那些中央銀行 - 即澳洲聯儲和挪威中央銀行 - 將維持這些“更高更久”立場多久。以最近的言論為準,目前看來,2024年澳洲聯儲和挪威中央銀行的降息似乎遙不可及,儘管在鮑威爾等人開始降低聯邦基金利率之後,這種立場能否持續尚存疑問。如果是這樣,那麼澳元和挪威克朗將成為G10外匯市場中明顯的多頭,可能會在風險情緒繼續保持的情況下對低收益貨幣獲得最顯著的益處

最後,有一個不確定因素,那就是日本央行。在7月傳遞出比預期更加鷹派的信息後,宣布上調15個基點並計劃削減日本國債購買的上田行長留下了進一步緊縮的可能性,同時指出0.5%並非利率的“上限”。日元OIS曲線價格顯示,到年底只有11個基點的進一步收緊,這似乎有些不足,為日元升值留下了空間,因為日本與其他地區的利率差繼續收窄,即使套利解除似乎在目前階段基本完成

除了政策,市場還需要應對美國大選的問題。在對金融市場重要的政策領域 - 例如財政政策 - 特朗普和哈里斯展示出了驚人的相似之處; 主要是,二者都不太關心更高的政府支出、不斷上升的赤字或激增的政府借款。最重要的政策差異出現在監管領域 - 特朗普支持放鬆監管,哈里斯基本支持對美國企業實行更嚴格的規定 - 尽管這些差異的市場影響主要將在股票領域展現出來,而不是在外匯市場上

最後,有一個不確定因素,那就是日本央行。在7月傳遞出比預期更加鷹派的信息後,宣布上調15個基點並計劃削減日本國債購買的上田行長留下了進一步緊縮的可能性,同時指出0.5%並非利率的“上限”。日元OIS曲線價格顯示,到年底只有11個基點的進一步收緊,這似乎有些不足,為日元升值留下了空間,因為日本與其他地區的利率差繼續收窄,即使套利解除似乎在目前階段基本完成

除了政策,市場還需要應對美國大選的問題。在對金融市場重要的政策領域 - 例如財政政策 - 特朗普和哈里斯展示出了驚人的相似之處; 主要是,二者都不太關心更高的政府支出、不斷上升的赤字或激增的政府借款。最重要的政策差異出現在監管領域 - 特朗普支持放鬆監管,哈里斯基本支持對美國企業實行更嚴格的規定 - 尽管這些差異的市場影響主要將在股票領域展現出來,而不是在外匯市場上

Preview

在外匯領域,人們預計特朗普的勝利對美元將是一個膝跳式的積極影響,即使只是機械性地由於墨西哥比索和人民幣兌美元的顯著貶值。然而,外匯市場通常更關心政治穩定,而不是政府的特定效忠,這意味著一個分裂的政府情景——即贏得白宮的黨派並沒有總體控制國會——可能是最重要的短期負面美元結果。總的來說,正如“自上帝還是個男孩以來”一直如此,市場在準確定價政治風險方面一直不佳。因此,預期波動率和實現波動率可能會在11月的投票日大幅上升,同時外匯需求也可能加速增長,因為交易員尋求對其他地方的政治敏感頭寸進行對沖。

Pepperstone并不表示此处提供的材料是准确的,最新的或完整的,因此不应以此为依据。此处提供的信息,无论是否来自第三方,都不应视为推荐信息;或买卖要约;或要求购买或出售任何证券,金融产品或工具的要约;或参与任何特定的交易策略。我们建议该内容的任何读者寻求自己的建议。未经Pepperstone同意,不得复制或再分发此信息。