- English

.png)

We move past month-end rebalancing flows, Nvidia’s earnings, and US core PCE inflation without too much angst, with the stage set once again for traders to go into battle and attempt to take capital from weaker hands. Momentum around the event risks will build through the week, before hitting a crescendo on Friday as we navigate the US nonfarm payrolls (NFP) report. An event risk where traders need to carefully consider their exposures over the announcement and where a key macro debate on the extent of the first Fed cut in this cycle could be settled.

If Nvidia’s quarterly earnings report was the most ‘anticipated earnings report ever’, then this week’s NFP is equally impactful, and becomes one of the most anticipated economic data points for some time. Unlike Nvidia, there won’t be NFP parties held across the US, with punters celebrating wildly as the jobs numbers drop - sharing screenshots on their mobile trading platform on statistics that will be revised heavily 2, if not 3 times.

US data to navigate this week

US data comes in heavy this week, with ISM manufacturing and services both having the potential to move broad markets. Growth data is important, but with US Q3 GDP tracking around 2.5% (as implied by both the Atlanta and NY Fed nowcast models), traders may not de-risk portfolios too emphatically on a downside surprise, as perhaps they would when recession banter was more prevalent.

The greater focus falls on the US labour market, as the Fed has essentially guided that this is where they're looking most intently and will not tolerate any further weakness. As Jay Powell detailed at Jackson Hole “There is ample room to respond to any risks we may face, including the risk of unwelcome further weakening in the labour market”. Subsequently, if the labour market matters most to the Fed, it matters most to market players (and algo’s) too.

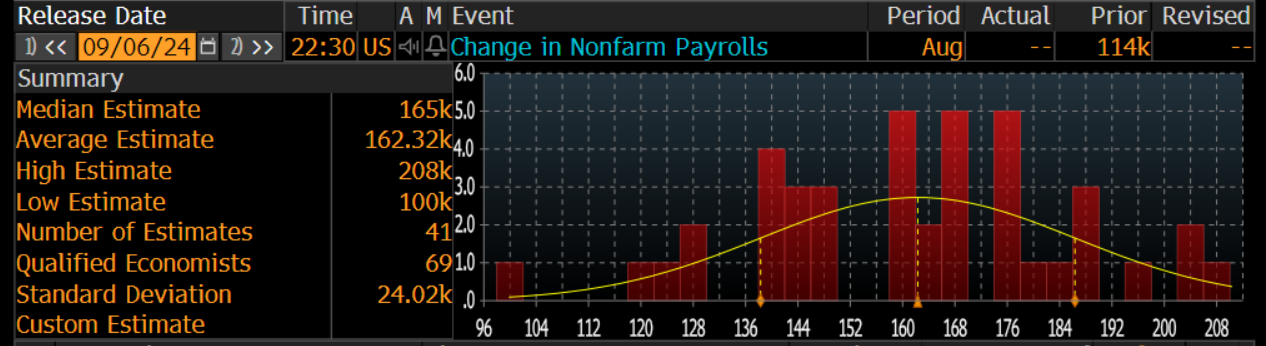

Distribution of NFP estimates

On the week we see labour market reads in the form of JOLTS job openings (consensus 8.10m openings), ADP payrolls (140k), Q2 unit labour costs (0.8%) and weekly jobless claims. However, it’s the NFP report on Friday that will arguably be the marquee risk on the week, with the median estimate from economists set at 165k jobs (the range of guesses is seen between 208k and 100k), with the U/E rate expected to tick lower to 4.2% and average hourly earnings eyed at 3.7% y/y.

US nonfarm payrolls to seal a 25bp cut or increase the odds of 50bp

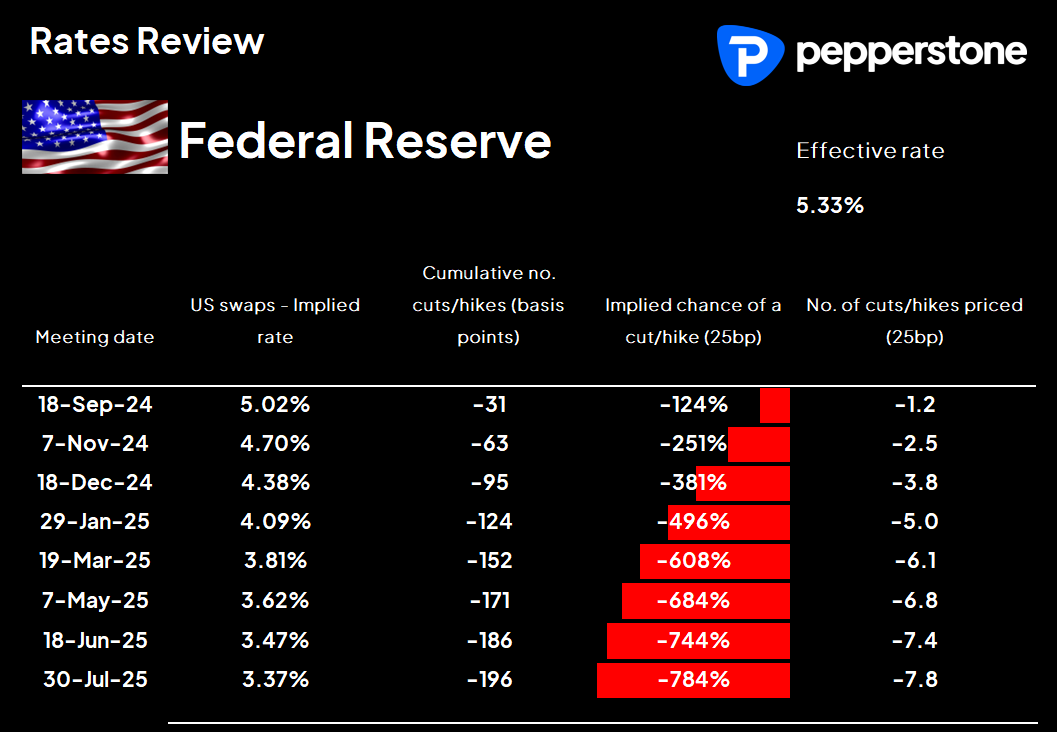

By way of market pricing, US interest rate swaps price 31bp of cuts (or a 25% chance of a 50bp cut) for the September FOMC meeting, and 95bp of implied cuts through to December. This is the first derivative of markets this week and changes in rate expectations should guide equities, the USD and gold.

A weak NFP, say below 130k with an unchanged read on the U/E rate, and we’ll likely see the rates market move closer to price a 50bp cut. A stronger NFP outcome than what’s priced and a 25bp cut will be the default position.

Another big consideration is that Fed Governor Waller speaks 2.5 hours after the NFP report, offering his outlook on the US economy. Traders will get a clearer sense of how Christopher Waller viewed the jobs report, and his views carry as great a weight as any within the FOMC’s ranks.

Tactically, good news should be good news for risky assets, and better numbers will likely lift equity, as it will the USD. A 25bp cut is the move the Fed really want to make, so further evidence that the US economy is headed for a soft landing, amid non-urgent rate cuts plays into a nirvana backdrop for risk.

A 50bp cut sounds positive for equity, but I am not so sure that would be the case and bad news on the labour front would likely lead to equity sellers – at least in the more cyclical areas of the equity market - and renewed USD selling.

Reviewing the higher timeframe charts

With the mentioned US data flow in mind, we review the big picture daily and weekly charts to gauge a probabilistic assessment for the potential near-term direction, which can skew how we see the balance of risk.

On the equity index front, the set-ups that offer the greatest potential for further near-term upside risk are seen in the S&P500, NAS200, NKY255, DAX30 and SPA35 – these scan as the strongest equity markets on the radar.

The S&P500 closed on its highs on Friday, but to get the large-cap index pumping I want to see an upside break of the recent consolidation range high of 5652 (5669 in the S&P500 futures). Should that materialise through the week new highs should come into play.

US banks and industrials are where the real outperformance is seen in equity, with the XLF and XLI ETFs both in a strong uptrend and attracting good flow. Big tech is lagging, notably after the disappointment of Nvidia not beating sales expectations by the GDP of a small country. However, buyers have stepped in to support Nvidia around $117.50, and should we see the share price at least track sideway, amid modest buying support in Apple ahead of next Monday’s ‘Glowtime’ event, then the rest of the market can do the heavy lifting and push the respective US indices higher.

The USD to rally into NFP?

On the FX side, the US dollar index (DXY) held the 28 December low of 100.61 well and has retraced towards 102, with EURUSD pulling back from 1.1200 to 1.1048, GBPUSD falling from 1.3266 to 1.3192 and USDJPY rising back above 146.00.

The Bank of Canada to cut by 25bp

USDCAD falls firmly on the radar, with the Bank of Canada meeting on Wednesday, where they are widely expected to cut rates by 25bp, with CAD swaps even implying a small premium that we see a 50bp cut. We also see the Canadian employment report on Friday, with expectations of 25k jobs created, and the unemployment rate eyed to tick up to 6.5%.

USDCHF has bounced off 0.8400 and momentum suggests the pair has the potential to push into 0.8600/20. The big risk this week is Swiss August CPI (due Tuesday at 16:30 AEST), where the market is pricing headline CPI to come in at 0.1% m/m / 1.2% y/y (from 1.3%) and core CPI at 1.1% yoy. Swiss interest rate swaps price 33bp of cuts for the next SNB meet on 26 Sept - so a weaker CPI print and the rates markets could imply a 50bp cut as the base case – A factor which could see USDCHF push towards 0.8550, with NZDCHF looking to firmly breakout and potentially bull trend.

In Australia, we see Q2 GDP on Wednesday, with expectations that the year-on-year rate of growth falls to 0.9%. We also hear from RBA Gov Bullock on Thursday with a speech at the Anika Foundation. In Europe, politics will get an increased focus, with the German states of Saxony and Thuringia headed to the polls with the ring-wing AFD party expected to poll well – a factor which could shape next year’s German Federal election. US politics also starts to kick into gear, with traders gearing up for the 1st live debate between Harris and Trump on 10 September. It still feels too early to express tactical views on the US, as the expression will be fighting the outcome of the NFP report – perhaps after the 1st debate between Trump and Harris we could see markets hold a greater sensitivity to changes in the polls, but even then, it feels like late September, early October will be a more fitting time to go hard on trading US election trades.

Good luck to all,

Chris Weston

Head of Research Pepperstone

Related articles

.jpg?height=420?quality=30)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients. Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.