For a while now, I’ve been harping on about how equities should remain underpinned amid the supportive policy backdrop, with market participants content to increase their exposure to riskier assets safe in the knowledge that the return of inflation towards the 2% target means that the ‘central bank put’ is both back, and more flexible than ever.

In other words, G10 policymakers can cut rates when they want, by how much they want, and provide as much liquidity as needed, wherever it is needed, as a result of seemingly winning the battle against double-digit inflation that has been waged over the last couple of years.

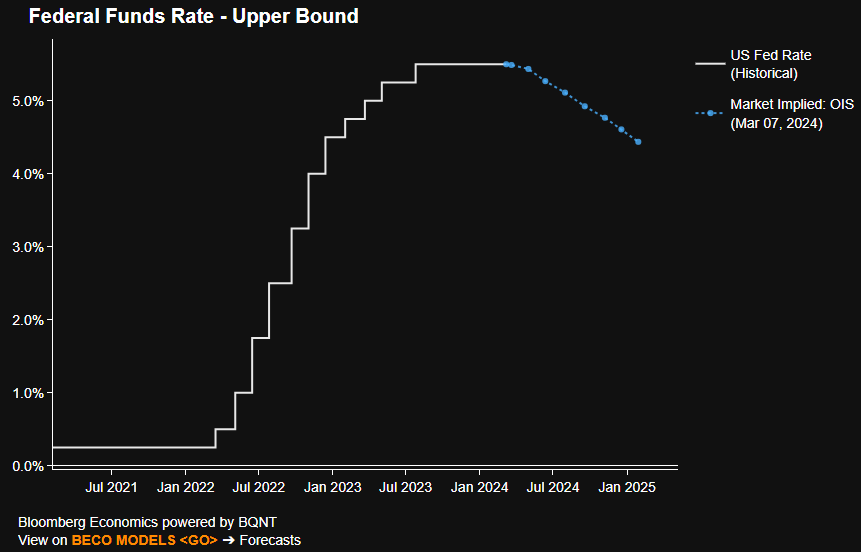

At the same time, I’ve also flagged how the biggest risk to this view is that central banks don’t deliver the prolonged easing cycle, and return to neutral rates, that consensus heavily favours, and which markets continue to price.

Over the last couple of days, there have been a few notable developments hinting that the probability of this risk occurring has risen a touch.

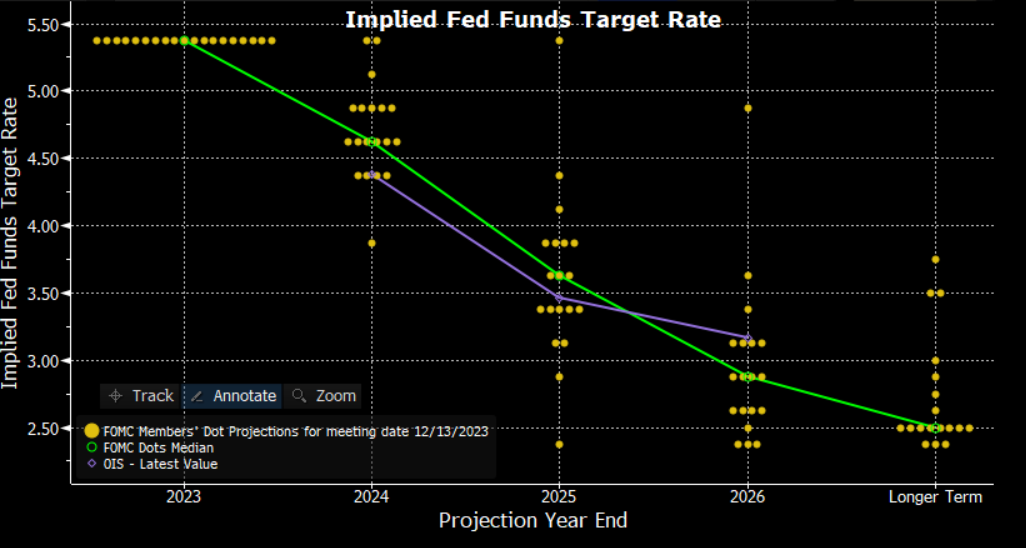

Firstly, Fed voter Mester - who, admittedly, retires midway through the year - noted that she is considering raising her forecast for the long-run fed funds rate. In other words, shifting her rightmost ‘dot’ on the below plot higher.

This is significant, particularly if her thinking is mirrored by other FOMC members, as a higher long-run estimate (essentially a proxy for where the FOMC see neutral being) would naturally necessitate a shorter and shallower easing cycle to move to a less restrictive policy stance. In other words, the higher the long-run rate estimate, the fewer cuts need to be delivered for us to get there.

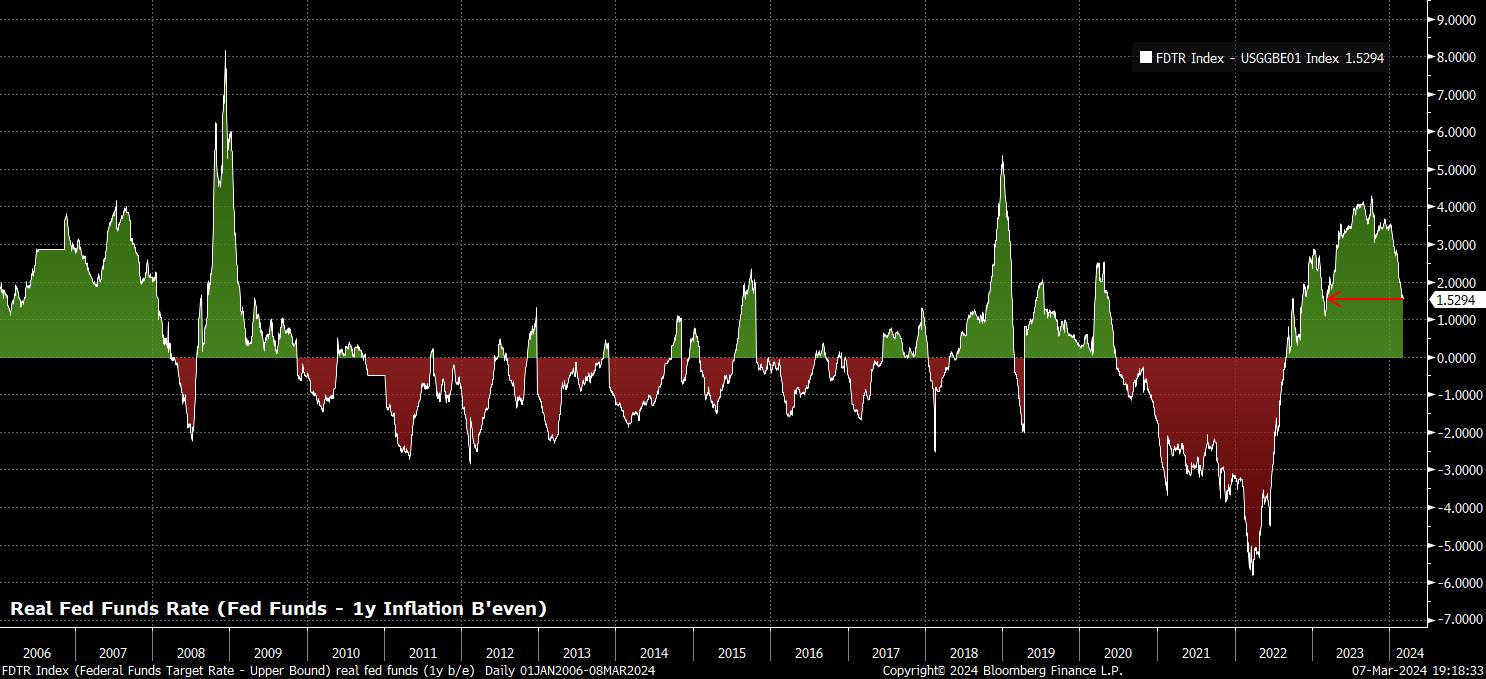

The second thing that has caught my eye is the real fed funds rate.

There are many ways of measuring such a concept, though Chair Powell’s preferred measure is to use the one-year inflation breakeven to perform the necessary adjustment. Using this measure, the real fed funds rate is at its lowest level in a year; by extension, making policy its loosest in twelve months.

Clearly, if policy is becoming looser, and the real fed funds rate is falling, there is less need, and likely significantly less desire, to begin to cut the nominal fed funds rate. If policy is becoming less restrictive without the FOMC doing anything, they are unlikely to want to add fuel to the proverbial fire by delivering a rate cut, particularly when certain corners of the market - e.g., crypto - are displaying signs of speculative frenzy and euphoria.

While these developments are notable, and risks that should remain on the radar, they are not enough for me to adjust my current base case that the path of least resistance continues to lead higher for risk.

However, a hot jobs report, and/or a hotter than expected inflation figure, will likely both serve to increase the risk that the Fed do not begin to refill the liquidity punchbowl quite as soon as markets would desire, while also raising the risk of a 25bp hawkish revision to the 2024 median dot at the March FOMC, in turn potentially being the catalyst for the next leg higher in the USD, and lower in Treasuries.

此处提供的材料并未按照旨在促进投资研究独立性的法律要求准备,因此被视为市场沟通之用途。虽然在传播投资研究之前不受任何禁止交易的限制,但我们不会在将其提供给我们的客户之前寻求利用任何优势。

Pepperstone 并不表示此处提供的材料是准确、最新或完整的,因此不应依赖于此。该信息,无论是否来自第三方,都不应被视为推荐;或买卖要约;或征求购买或出售任何证券、金融产品或工具的要约;或参与任何特定的交易策略。它没有考虑读者的财务状况或投资目标。我们建议此内容的任何读者寻求自己的建议。未经 Pepperstone 批准,不得复制或重新分发此信息。